Category: Entrepreneurs

Automate Salary Payments

You may be all-too-familiar with the process and time spent dealing with payroll and HR: emails, telephone calls, attachments, more emails to employees, setting up bank payments…the list goes on. Large businesses will have segregated duties, with an HR lead responsible for managing joiners and leavers and holiday requests, an Operations Manager for coordinating and communicating shifts, a Payroll Manager and a Financial Controller. For small-to-medium sized businesses, the responsibility often lies with the managing director. In this regard, there are some fantastic tools to make managing your team more pleasant and more efficient, including the new way to automate salary payments.

Paying salaries

The latest integration to the cloud payroll ecosystem automates the payment of staff salaries. Currently, we prepare a BACS payment file which many employers upload to their online banking facility for processing onwards payments. The latest payments platform goes a significant step further and allows us as your accountants to make payroll payments, linked to your payroll information, shortly after the payroll is approved, saving you precious time, removing manual processes, and eliminating costly errors. The seamless workflow is protected by two factor authentication and payments are processed through a highly secure and compliant network. This solution benefits all employers with a high headcount and who pay their staff via bank transfer.

Employer and Employee Portal

By integrating with our payroll software in the cloud, we can streamline the way you communicate payroll information to us, including hours worked, holiday days taken, bonuses or new starters. A browser- or app-based Employer Portal allows you to enter relevant information, store and organise documentation (including payroll reports which we prepare) and make final approvals. We can email your employees their payslips directly, or even grant them access to the Employee Portal, where they can retrieve payslips (including past payslips), submit holiday requests, enter starter data…etc. This functionality benefits businesses in all sectors, as it is centred around improving the information flow between the employer, the employees and the accountant.

Rota Management

If your business requires organising shift patterns for your staff, we can help you implement software which helps you schedule rotas, optimise wage spend, record attendance and approve timesheets for payroll. Your employees would receive pop-up notifications and would log their check-in and check-out times in the app. The app can then produce weekly reports showing hours worked and wages due. There are also built in features such as overtime pay and GPS, which would ensure that employees can only log in when actually present. We have found this software to be particularly helpfuly for hospitality businesses and beauty salons.

How much does it all cost?

The payment integration and cloud hosting is priced based on the number of active employees, and the efficiency saving will tend to outweigh the fee for a payroll with at least 4 employees.

Our Information Sheet sets out a full list of our integrated Payroll and Pensions services.

Whether you’re an existing client or don’t yet use our services, we would be pleased to help you. Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Hair Salon Business Model: which style suits you?

As a hair salon or barber shop owner, you aim to run your business in a way that maximises revenue, reduces costs, and ensures a good working relationship with your staff and customers. It is important to choose the right model that suits your business needs from the outset. We discuss below three different models of business:

- Full operation, whilst operating:

- a PAYE scheme

- a self-employed model for hairdressers

- Chair rental

- charging a fixed weekly rent to barbers

- charging a percentage of the chair’s takings

- a combination of a and b

- Shop rental

Full Operation

Full operation is the most involved and therefore carries the capacity for highest profits. This model also incurs the highest administrative costs, both in terms of money and time, including:

- Paying over 20% VAT on your sales if turnover exceeds £85,000

- Maintaining a payroll service to your staff

- Carrying out senior management responsibilities

Self-employed basis

As senior manager, you could continue operating the business, whilst moving some of your staff to a self-employed basis. The benefit of transitioning could save money in the following ways:

- No legal obligation to pay for sickness, maternity or holiday

- You avoid paying Employer’s national insurance

- There is no need to worry about auto enrolment pensions or make contributions

Should you pursue this model, it would be worthwhile implementing a service contract with the freelancers, to ensure that both parties’ expectations are understood. Of course, the risk of a barber turning up late, taking a day off or poaching clients for their own business remains. You should take on full advice, including with respect to legislation around self-employment.

Internal Controls

If you are not present at the salons throughout the day, it would be worthwhile implementing Internal Controls. These should be considered especially if you will continue to operate the salons, or even if you plan to sub-let at a variable rate dependent on performance. Internal Controls for cash sales and collections include:

- Reconciling till rolls to cash collections each day.

- Reconciling cash collections with banking and sales records each day.

- Restricting the receipt of cash and the recording of sales by making sure that only one person is in charge of the cash register.

Internal Controls to accurately track employee time should be considered if you are paying your staff per hour, either as employees or subcontractors. To help you accurately monitor and control employee timesheets, we have helped our clients implement an app-based time management software which you or your management could use to organise rotas.

Chair rental

There are three models to renting out chairs:

- Charging a fixed weekly rent to the freelancer

- Charging a percentage of the chair’s takings

- A combination of a and b

With option 1, if there is a high volume of customers for a particular chair you will lose out on sales as the freelancer will take all of the earnings. Option 2 avoids this problem, however if the freelancer doesn’t turn up for work then you lose out on rental income compared to the first model. A combination of the two methods is arguably the best way forward, however it would require monitoring of sales figures. The incentive agreement should be set at a level where the freelancers have the potential to make more money than they currently do.

You would need to charge VAT on rental income should your turnover exceed £85,000. A non-VAT registered freelancer would then suffer the VAT. Of course, the barber may also seek VAT registration, depending on his or her particular circumstances.

Compared to the full operation model with staff there will be no wages, national insurance and pensions costs however sales will be limited as per your agreement with the freelancers. Should you pursue this model, it would be worthwhile:

- implementing a service contract with the freelancer. It would be important to draft strong payment terms to avoid the risk of arrears.

- implementing an EPOS till system to give you full visibility of sales (important with incentive agreements).

- considering whether you would allow freelancers to sell their own products, or take a commission from your sales.

An additional risk compared to an employee-based model is that freelance workers may come and go, thereby requiring more management time to maintain occupancy.

Shop rental

This option is the least involved. If you do not foresee a pick-up in footfall in your salon, you may consider subletting your salon and collecting the passive income. You should bear the following points in mind:

- First check whether your lease allows you to effectively sub-let the premises.

- Should turnover increase more than you anticipate, you will not be sharing in the upside.

- Should you eventually sell the business, your eligibility to pay the Entrepreneurs’ Relief rate of CGT of 10% will be in jeopardy.

Summary

- The full operation model has the greatest potential for maximising profitability but carries the highest level of administrative costs.

- Internal controls regarding hours worked and wages paid are paramount, especially if you will continue to be directly involved in the full operation of the business.

- If you decide to base your business model around working with freelancers, it is important that both parties’ duties are understood (owner and freelancers). A service contract between parties is key.

- If the chair rental model is pursued you will need to charge VAT if rental income exceeded £85,000, which a freelancer could then suffer.

- The chair rental model is the most cost-effective option, but you risk losing out on revenue if there is a high level of footfall.

Whether you’re an existing client or don’t yet use our services, we would be pleased to help you. Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

The Taxation of Inter-company Loans

Under the right circumstances, which can of course be shaped, intercompany loans are an effective means of funding further profit or not-for-profit motives. Consider Mr Trader, who is director and sole shareholder of Company T, a trading company. Company T has grown with accumulated profits in excess of £2m, matched by substantial cash balances. Mr Trader has decided to set up a not-for-profit organisation, ReMobly Ltd, aimed at rehabilitating injured athletes back into competitive sport. In addition to Mr Trader, two other directors will be appointed to the board of ReMobly Ltd and each of the three persons will own 33% of the ReMobly Ltd share capital.

ReMobly Ltd is seeking to raise capital to begin its operations and Mr Trader is considering the most apt means of lending money to the not-for-profit organisation. There are three issues which spring to mind…

Loans to participators

In view of the large cash balances that have accumulated in the company, Mr Trader considers lending money from Company T to ReMobly Ltd. CTA10/S455 applies to loans/advances made by a close company to its participator, or an associate of its participator. Broadly, where a close company makes any loan to an individual who is a participator (or an associate of a participator) in the close company, then the close company is due to pay tax under CTA10/S455. The not-for-profit is not classed as an associate of Mr Trader (so far as section 448 of Part 10 of the Corporation Tax Act 2010 is concerned), therefore the loan can be made by Company T without corporation tax implications under CTA10/S455.

It is also important to analyse CTA10/S459, which applies if there are arrangements made by a person whereby a close company makes a loan or advance that is not subject to tax under CTA10/S455, and another person makes a payment to a relevant person who is either a participator of the company or an associate of such a participator. In this case there is a proposed “loan or advance” from a close company. However, there is not then a payment by a person other than Company T to a relevant person who is a participator in Company T or is an associate of such a participator. Indeed ReMobly Ltd is not a relevant person who is an associate of Mr Trader, because a relevant person has to be an individual or a company acting in a fiduciary or representative capacity (CTA10/S455(6)). Therefore the loan can be made without corporation tax implications under CTA10/S459.

Loan write off

There is a possibility that the future activities of ReMobly Ltd will be inadequate to allow for the repayment of the loan made by Company T, under the terms of the loan agreement. If both parties are companies and both are found to be under the common control of another person, company or individual, at any time in the accounting period, then no bad debt relief will be available on the release of the loan, and no taxable credit will arise to the company whose indebtedness is forgiven. Company T and ReMobly Ltd are not under the common control of another person and are therefore not considered to be connected. The debit for the loan write off will be allowable for Company T (most likely as a non-trade loan relationship deficit). The corollary is that a taxable credit will arise to the not-for-profit.

Anti-avoidance

The main anti-avoidance rule will also need to be considered in FA 1996, Sch 9 para 13, the ‘unallowable purposes’ rule. This will deny relief for so much of a debit where the loan or part of the loan is attributable to an unallowable purpose. An unallowable purpose is any purpose which is not amongst the business or other commercial purposes of the company, Company T. If taken literally, this would seem to be cast fairly widely. In general however, if the loan relationship rules are seen to be fairly applied to both parties, HMRC seem content in leaving matters undisturbed.

Whether you’re an existing client or don’t yet use our services, we would be pleased to help you. Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

EIS Tax Relief for Joint Investment

The following scenario often arises with our client Mr Investor, who is considering investing in an early-stage business. Wonderful Ltd is an established FinTech company which has developed a track record of an established user base, consistent revenue figures and other key performance indicators. Wonderful Ltd is now seeking to raise Series A funding of £1.5 million in order to further optimize its user base and product offerings. Mr Investor has received an Investment Memorandum for the funding round and is considering allocating a small proportion of his investment portfolio. Mr Investor has asked his accountant to run through the Investment Memorandum with him and has identified five reasons why he wishes to invest. Being an early-stage business, Mr Investor acknowledges that the investment is inherently high-risk, but he really believes in the founder Mrs Wonderful, who attended the same university. The generous Enterprise Investment Scheme (EIS) tax breaks “cushion” the risk element of the investment (see below) but nonetheless, the minimum investment of £75,000 is punchy for Mr Investor.

Mr Investor has an idea. Can he pool together capital from two other friends in order to meet the £75,000 minimum investment? Will each investor still be eligible for the EIS tax relief for joint investment?

Joint Investment – A Problem Shared is a Problem Halved

In short, there is a way to pool funds in order to meet one investment clip of £75k. EIS relief is available for an individual who makes the subscription on his or her own behalf, with two notable exceptions:

- Individuals who use another person as a nominee to subscribe for the shares, or be registered as the holder of them, on their behalf, are treated as themselves being the subscriber.

- Individuals who invest jointly with others, with the result that the subscribers are in law acting as bare trustees (whether for themselves or for others), are themselves as individual beneficiaries treated as being the subscribers.

Mr Investor can therefore form a bare trust with his friends (as in point 2) in order to make a direct investment jointly. Where shares are issued to a bare trust on behalf of a number of beneficiaries, each beneficiary is treated as having subscribed, as an individual, for the total number of shares issued to the bare trustees divided by the number of beneficiaries. This creates an important limitation in that each of the three friends should invest an equal percentage in Wonderful Ltd.

Paperwork

Wonderful Ltd should provide each subscriber form EIS3 showing the total number of shares subscribed for on Page 1 of the form. Form EIS3 Page 3 should show the amount on which each owner is entitled to claim the tax relief for the shares, that is the fractional amount of the total subscribed.

Tax Relief?

Whilst joint investment does not preclude EIS tax relief, Mr Investor and his associates must of course check that all the other EIS eligibility criteria are met for EIS tax relief to apply. Mouktaris & Co can provide a checklist of questions to ask in order to determine whether tax relief under EIS is available to an investor in shares. The target company may produce an Advance Assurance document to potential investors demonstrating that HMRC accepts the investment under the scheme, however Advance Assurance will not tell you if an investor would meet the conditions of the scheme.

EIS Investment Funds

A different route (via point 1 above) would be for Mr Investor to invest via an EIS investment fund, which is structured as a nominee vehicle which invests funds in EIS-qualifying companies on behalf of investors. This vehicle would provide Mr Investor with a more diversified risk exposure to early-stage businesses, as his £25,000 investment would be spread across a number of target companies identified by the fund manager. Wonderful Ltd may seek to market its strengths to the EIS investment fund manager so as to be included in the fund’s equity holdings. So in fact Mr Investor could in the future invest in Wonderful Ltd through an EIS investment fund without necessarily being reliant on his friends’ capital.

EIS for Investors: Advantages

- As a reminder, EIS investors receive the following benefits as a result of participating in the scheme:

- A 30% income tax break against the amount invested

- No capital gains tax (CGT) to be paid on any profit arising from the sale of the shares, as long as they are held for at least 3 years

- Payment of CGT can be “rolled over” if the money gained is invested through EIS. The investment must be made 1 year before or 3 years after the gain occurred

- No inheritance tax is payable provided shares are held for at least 2 years

- If the shares are sold at a loss, the loss can be offset against any income tax in that year or the previous year

Whether you’re an existing client or don’t yet use our services, we would be pleased to help you. Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

How to Invest Business Profits

With many entrepreneurs accumulating cash in business accounts, the question of “how to invest business profits?” is a favored topic when planning.

Entrepreneurs work hard for their businesses and this short article explores how business funds can work hard- or most effectively, for entrepreneurs.

Let’s take the following scenario: your business is profitable and has accumulated cash. During the years of trading, you have typically drawn an annual salary and dividends of £45,000, a point at which you are paying the basic rates of tax. Now with a stockpile of cash in the business, there are two options through which to invest. Should you personally draw additional funds from the company to invest, or alternatively should you invest from within the corporate structure?

Assume in both cases there is a £50,000 cash surplus in the company. Assume also that this happens every year for the next 10 years.

Personal investment through your ISA

To take the money out of the company, you would pay dividend tax of 32.5% upfront. You (and perhaps your partner) could then invest your money tax-free, say in an ISA wrapper, in which your combined ISA allowances are currently £40,000.

Investment through your Company

Investing the money within the company would mean no upfront dividend tax of 32.5%. You would instead pay corporation tax on the investment income and gains annually, with the caveat that dividends received from stocks and shares are mostly exempt from corporation tax. This is a considerable advantage.

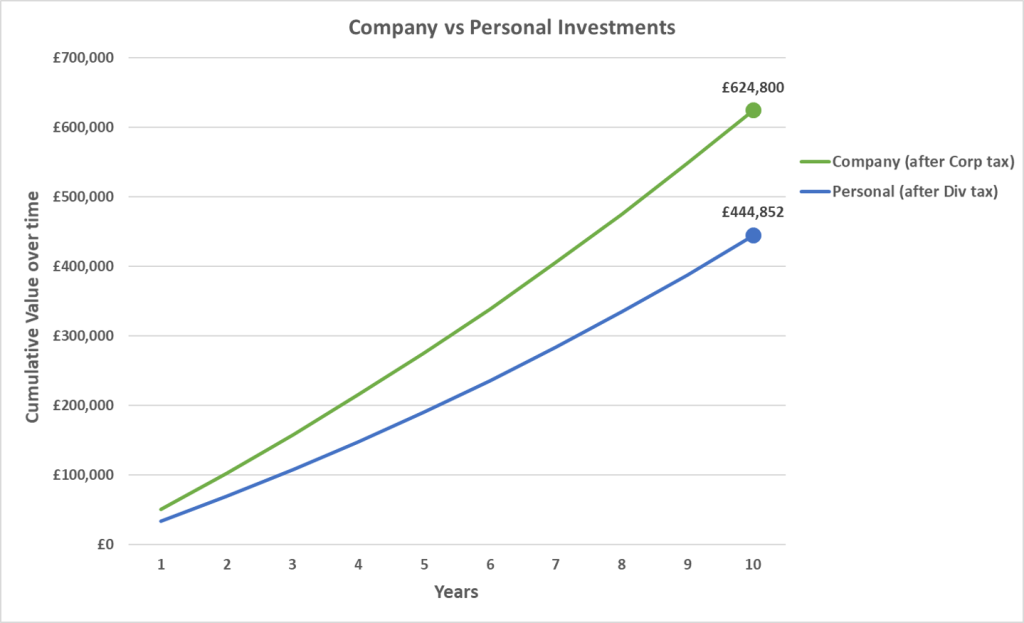

Let’s see how the two strategies fare:

As you can see, investing the money in a limited company yields approximately £180,000 more over a ten-year time horizon. The cost of paying the dividend tax upfront outweighs the benefit of tax-free personal investments. Why should you lose out?

Compounding evidence

You will notice immediately from the graph above that investing your company’s profits in the corporate vehicle, without paying dividend tax, allows the investment to accumulate, or compound, at a faster rate, even after paying corporation tax on investment income and gains.

Sure, if you do not draw the surplus funds from your company you may need to take a 32.5% dividend tax rate hit at a later date, but in the interim you will have generated greater income through compounding.

Caveats

Here we assume constant tax rates at the points of execution, income and realisation. It would be unwise to speculate on domestic policy, but current political trends and economic philosophy may see a conservative government try to enforce its stronghold on previously labour heartlands. Corporation and dividend tax rates could well rise before they fall.

You may find that transaction costs are slightly higher for corporate accounts, chipping away at annual returns. You will need to shop around harder for a broker. Equally personal brokerage accounts tend to be more insurable than corporate accounts.

Investing through a Limited Company

If the preference for investing through a Limited Company has been established, so should the mechanism through which to do so. Yes, you could simply open an investment account for the existing trading company, however there are several reasons why a designated investment company is superior:

- If the trading company runs into legal issues, the investment company will be protected.

- The trading company can be sold off as a standalone vehicle without the need for complex restructuring.

- An investment company will have minimal expenses and overheads, meaning it will be easier to administer for tax purposes (no VAT or payroll requirements).

- A trading company shouldn’t start investing in activities outside its core functions as it could end up becoming reclassified. This may carry tax implications, especially if Entrepreneurs’ Relief is sought.

Whilst the trading company is often the vehicle in which profits have been generated and accumulated, there are tax neutral ways of shifting funds to an investment company, such as lending the cash surplus. There is no obligation to pay back the loan and one can be the sole director of both companies.

A Holding Company

A holding company structure that owns operating companies and receives dividends is favourable. The holding company can own shares in the subsidiary trading companies and can provide centralised corporate control. Additionally, no taxes would be incurred when the trading company is sold.

Special Purpose Vehicle (SPV) for Property

If you want to invest in property it may be a better idea to set up an SPV. This is often a requirement from buy-to-let lenders. If you are looking to acquire a primary residential residence however, personal ownership is often the best way to go.

Don’t let the tax tail wag the investment dog

Your investment goals will seek a level of risk and return that you are comfortable with, regardless of the structure through which you pursue them. The tax wrapper is the “cherry on the top”, though worth a certain percentage of your annual returns. Contact Mouktaris & Co Chartered Accountants for an accountant who understands your investment strategy and can help you plan accordingly.