Category: Corporate Tax

Spring Budget 2024 – The leaked and leaky Budget

Spring Budget 2024

The Chancellor managed to find some optimism in the deteriorating economic forecasts, as most Chancellors, of whatever political hue, seem to do before an election. Mr Hunt announced a further 2% cut to national insurance, although it appears that the current budget deficit and the anticipated fall in inflation to 2% did not arrive in time to arm the Chancellor with the fireworks needed to queue an election. With this in mind, the Autumn Statement 2024 is now likely to be the “main event”, if we may, for the Conservatives to bring in a final raft of measures, including perhaps Mr Sunak’s long-forgotten “promise” to slash the basic rate of income tax from 20p to 19p by 2024.

Indeed the speech from Mr Hunt did not feel like a genuine election push; he rather serenaded the opposition and there was an absence of an impassioned pre-election tone. The Conservatives have accepted this election will go very late, or perhaps they have accepted that they will go down with dignity (and cheques that will bounce back).

Whereas in years gone by ministers responsible for leaks to the press resigned on the spot, party politicians have warmly embraced the new age of “populism” and the Budget was leaked, in drips and drabs over the course of the past few days, to various news organisations.

Headlines and commentary as follows…

Spring Budget 2024

Personal taxes

- Tax Rules for non-UK domiciled individuals – from 6 April 2025, the current remittance basis of taxation will be abolished for UK resident non-domiciled individuals. This will be replaced from 6 April 2025 with an elective 4-year foreign income and gains (FIG) regime for individuals who become a UK tax resident after a period of 10 years of non-UK tax residence. There will also be transitional provisions for non-doms currently paying tax on the remittance basis, including a 12% tax rate on foreign income arising before April 2025 but brought into the UK in the tax years 2025/26 or 2026/27. Do the Conservatives now feel that the abolition of these breaks will not result in a mass exodus? In practice, looking at the polls and the fairly imminent election, this particular measure won’t be in place before there is a change in government and any actual amendments to the regime are likely to be quite different.

- High Income Child Benefit Charge (HICBC) – the HICBC income threshold will be raised from £50,000 to £60,000 from 6 April 2024, and the taper will be extended up to £80,000. A migration to a system based on household rather than individual income is planned by April 2026.

- ISAs – introduction of a UK ISA with a new £5,000 allowance, in addition to the existing ISA allowance.

National Insurance contributions – whilst any “tax” cut is welcome, one must recall that the same percentage increase was levied by the same party in order to fund “social care”. Have then, the problems of social care been solved? Or do they no longer matter? The state of our public services will quite possibly be the biggest challenge of the next elected party.

- Class 1 – a cut to the main rate of Class 1 employee NICs from 10% to 8% from 6 April 2024.

- Class 2 & 4 NICs – a further cut of 2 pence to the main rate of Class 4 self-employed NICs from 6 April 2024, taking this to 6% of profits. The consultation to abolish Class 2 NICs to continue.

Property

- Capital Gains Tax (CGT) – a reduction to the higher CGT rate for residential property disposals from 28% to 24%. The change will take effect for disposals that take place on or after 6 April 2024. The lower rate of 18% will remain unchanged. For those with second homes, perhaps a “softener” to finance the VAT to be paid on school fees after the election?

- Furnished Holiday Lettings (FHL) – Were the tax breaks really responsible for exacerbating housing pressures of tourist areas to the detriment of local residents (many of whom also happen to be voters in marginal seats)? Draft legislation to be published in due course, but from April 2025, the generous tax advantages afforded to FHLs operating as either individuals or corporates will be abolished.

Excise and Duties

- VAT

- The VAT threshold will increase to £90,000 from 1 April 2024, and the level at which a business can apply for de-registration will increase from £83,000 up to £88,000. It is good to see the VAT threshold increasing, but we can’t help but ask Mr Hunt: why not go big and move the threshold to say £100,000? We feel that this would move the stifling cliff edge quite some distance for smaller traders; plus, a higher threshold could have taken out a large swath of businesses and reduced demand on HMRC, who are clearly struggling to perform.

- Also, the VAT implications for the private hire vehicle sector will be examined in April 2024, with potentially full expensing to give 100% corporation deductions for qualifying capital expenditure.

- Stamp Duty Land Tax (SDLT)

- First Time Buyers’ Relief will be extended to individuals who use nominee and bare trust arrangements when buying a new lease over a dwelling that they intend to use as their main or only residence.

- Abolition of Multiple Dwellings Relief, a bulk purchase relief within the SDLT rules available on the purchase of two or more dwellings.

- Vaping Duty – a new duty on vaping products will be introduced in October 2026, details on the design and implementation to be announced.

Business taxes

- Energy Profits Levy – the “temporary” tax on oil & gas profits introduced in 2022 has been extended to 1 March 2029. However, alongside this extension is a separate measure which will switch off this tax automatically if the average price for both oil & gas drops below certain thresholds.

- Creative Industries – New permanent rates of relief (40% and 45%) for theatre, orchestra and museums and galleries exhibition tax, and additional support for independent film through a new UK Independent Film Tax Credit at a rate of 53% for films with budgets under £15 million that meet the conditions of a new British Film Institute test. Plus, a 5% increase in tax relief for UK visual effects costs in film and high-end TV, under the Audio-Visual Expenditure Credit (AVEC).

- R&D – an expert advisory panel to support the administration of research and development (R&D) tax reliefs.

Tax administration

- Cryptoasset Reporting Framework (CARF) – the government has launched a consultation to seek views on how best to implement the Cryptoasset Reporting Framework and Amendments to the Common Reporting Standard.

Visit our Budget Highlights and tax data for a summary of the Spring Statement 2024.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Payrolling Benefits

What is a Benefit in Kind?

Benefits in kind (BIKs) are benefits that employees or directors receive from their employer which aren’t included in their salary or wages. BIKs are popular elements of many people’s salary packages and can be used by an employer to structure an effective and tax-efficient salary package.

Some BIKs aren’t taxed, but most are. As well as the impact on an employee’s personal tax, national insurance contributions are payable by companies, such that the tax treatment is broadly similar to that when paying a salary (although employer pension contributions are not due on BIKs).

What is Payrolling Benefits?

We are encouraging employers to take advantage of using payroll facilities for the purpose of reporting expenses and benefits. Rather than filing an annual P11D, an employer can report and deduct tax on the value of benefits provided to an employee each pay period though PAYE. This means doing away with the end of year P11D process, as taxes are submitted in real time.

HMRC will issue an employee with a new tax code to automatically account for the benefit provided and charge the correct amount of tax, in real time.

An employer will still need to complete and submit a P11D(b) form and pay Class 1A National Insurance on the value of the benefit provided to employees.

Employer Duties

Once an employer has registered to payroll benefits, they must give employees written notice explaining which benefits will be payrolled, the cash equivalent of the benefits, and details of benefits that will not be payrolled. Details on communicating with existing and new employees are set out on gov.uk.

Working out the taxable amount of a benefit in kind

The taxable amount of the benefit is the same as its cash value. This is then divided by the number of paydays the employee has in each pay period, so that tax is applied appropriately.

What if the value of the benefit changes?

It’s fairly common for benefits such as gym memberships and car costs to change during the year. If this happens, it’s simple to process the change. You must however ensure to keep us updated with changes when you communicate with us in the normal course of operating payroll. Examples of changes to the value of the benefit provided to the employee include:

- a change in price of the benefit, such as an increase in insurance premium

- a change in the number of days worked by the employee, including if an employee leaves

We recommend you discuss any benefit you plan to offer your company’s directors and employees with one of our expert accountants. As you can see, the rules around benefits in kind are complex and each example needs to be looked at based on its individual circumstances to see if any tax is payable by the employee and/or your company.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

ATED Valuation Update for 2023/24 return

ATED Update

Certain companies owning UK residential property need to submit an Annual Tax on Enveloped Dwellings (ATED) return every year. ATED is payable by companies that own properties valued at more than £500,000 if none of the various reliefs apply.

Valuation dates and the 2023-24 ATED return

Valuation dates are relevant for determining a company’s ATED position. It is the value of the property on the most recent of these valuation dates which is relevant for determining the annual chargeable amount due on the property. The previous “valuation date” was 1 April 2017, which applied for the 2018-19 ATED year and all ATED years up to and including this 2022-23 ATED year.

For the forthcoming ATED year 2023-24 and all ATED years up to and including the 2027-28 ATED year, ATED charges will be rebased to 1 April 2022 property values and so a revaluation of properties will be required as at 1 April 2022. ATED Returns are due within 30 days of the start of the relevant chargeable period i.e. by 30 April 2023 for the 2023/24 period.

Property Valuation

If a revaluation has not been carried out on properties, directors should consider doing so as a matter of urgency to ensure that future ATED liabilities are based on the correct valuation. This is especially important if the property is valued close to the ATED bands detailed below. Even if the company’s property is currently relieved from ATED, it would be prudent to have a 1 April 2022 valuation should circumstances change.

Property values were particularly volatile post-Brexit and there were instances where values actually fell when the April 2017 revaluation exercise was undertaken. Given the effects of the coronavirus pandemic on property values, similar considerations may apply when the 2022 valuation exercise is undertaken, although different considerations will apply to different regions and properties.

Directors can ascertain the property value or a professional valuer can be used. Valuations must be on an open-market willing buyer, willing seller basis and be a specific amount.

ATED Annual Chargeable Amounts

Annual chargeable amounts can be found on gov.uk.

Pre-return banding check

If your property falls within 10% of the above value bands and you can’t take advantage of a relief to reduce your ATED charge to nil, we can ask HMRC for a pre-return banding check (PRBC) in advance of submitting your return. If HMRC complete your PRBC after you’ve submitted your return and they don’t agree with your valuation, you’ll need to complete an amended return.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Spring Statement 2023

Back to the Future

Following the “Growth Plan” mini budget delivered by Kwasi Kwarteng on 23 September 2022, Jeremy Hunt took centre stage for the second time on 15 March 2023 to deliver a…”Budget for Growth”.

Fiscal policy can be assessed in three measures: efficiency, effectiveness and equity and whilst the announcements were fairly safe, a handful are poorly timed or likely to be ineffective:

- During an interview with BBC Radio 4 when defending the scrapping of the £1.073m tax-free cap on the lifetime pension allowance, Jeremy Hunt remarked that “we do know that we have a shortage of doctors and we know we have a very big backlog, and that is why we’ve decided this [scrapping of the lifetime pension allowance] is a very important measure to get the NHS working”. Said whilst junior doctors are on prolonged strike over pay and conditions; we suspect that Mr Hunt may have skipped his situational judgement module at Oxford!

- The Spring Budget is designed to “…break down barriers to work, unshackle business investment and tackle labour shortages head on”. Whilst the headline measure of 30 hours of weekly free childcare is a great and targeted initiative, Mr Hunt is making some parents wait up to 2 years and 5 months for the benefit.

As regards equity, the Budget is fairly safe and business-focused, but it does not appeal particularly to small and medium-sized enterprises (SMEs) who now face a rise in corporation tax and who are unlikely to benefit from the full expensing capital allowances policy. In addition the chancellor has failed to take any action to make it easier for small firms to recruit people locked out of the labour market.

In other news regarding:

- Childcare: Extension of 30 hours of weekly free childcare to cover nine-month to two-year-olds for working parents, to be fully phased in by September 2025.

- Taxes: Increase in corporation tax from 19% to 25%.

- Capital allowances: A “full expensing capital allowances policy” under which companies can write off qualifying expenditures against taxable profits.

- Research & Development: From 1 April 2023:

SMEs will received an increased rate of R&D relief from HMRC: £27 for every £100 of R&D investment if they spend 40% or more of their total expenditure on R&D.

the rate of the Research & Development Expenditure Credit (RDEC) is increased from 13% to 20%. - Energy: The government will keep the £2,500 annual cap on household energy bills in place for a further three months until June. Fuel duty has also been frozen for another year.

- Local growth: Tax incentives and other benefits for 12 investment zones across UK cities and towns worth £80m each over five years.

- Pensions:

- The annual tax-free pension allowance will be increased from £40,000 to £60,000.

- The Lifetime Allowance – previously set at £1.07m – will be abolished. The 25 per cent tax-free lump sump will though remain pegged to the current lifetime allowance, rather than 25 per cent of your whole pot.

- The money purchase annual allowance (MPAA) currently capped at £4,000 or £3,600 per tax year, has been increased to £10,000.

- Energy: Investment of £20bn over the next 20 years in carbon capture and storage projects.

- Pubs: A pint will become 11p cheaper but a glass of wine will cost 45p more from August.

Visit our Budget Highlights and tax data for a summary of the Spring Statement 2023.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Autumn Statement 2022

Taxing Times

In the latest decisive swoop of indecisiveness, Jeremy Hunt performed a 180 degree turn from the Mini Budget delivered less than two months ago by his predecessor. If the Mini Budget was dubbed “The Growth Plan”, can the Autumn Budget also be a plan for growth?

It was a step in the right direction: re-implementing fiscal discipline in an effort to re-galvanise trust in HM Treasury. Notwithstanding, it’s disappointing that fairer and more creative means of collecting taxes were not applied, rather than manipulating the tax bands in a move which fiscal-drags one and all. The 40% band no longer applies to the wealthiest. The capital gains tax rates on investment income are still only 50% of those paid on working income.

There were surely opportunities missed to rebalance the tax-system in a much-needed fairer way. Especially now in the face of a looming recession – or potentially depression, when the smallest tweaks in taxes and spending will have knock on effects on the amount of money that is spent on our high streets.

Taxes aside, there is risk of a continued disintegration of public services – this will come home to roost in two years if inflation continues its current trajectory amidst public spending cuts of £28bn.

Visit our Budget Highlights and tax data for a summary of the Autumn Statement 2022.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

One Entertains: Tax Allowances for the Platinum Jubilee (and other Entertainment)

With the dust still settling on the Mall following a triumphant celebration of Her Majesty The Queen’s Platinum Jubilee, one may begin to consider the tax deductibility of hosting Diana Ross, Ed Sheeran and the like – a figure reported to be around £28m.

As a general rule for tax, expenditure on entertainment or gifts incurred in the course of a trade or business is not allowed as a deduction against profits, whether incurred directly or paid to a third party such as an events organiser. HMRC are not however completely devoid of holiday spirit and provided conditions are met, certain types of entertainment are allowable. Hurrah.

Promotional Events

Events which publicise a business’ products or services are not deemed to be entertaining expenditure and so direct costs are allowable for tax if they meet the “wholly and exclusively” test. The cost of related food, drink or other hospitality is however disallowed. For example if a car manufacturer organises a golf day at which test drives are available, only the direct costs of the test drives and of any publicity material provided are allowed, together with any immaterial costs such as teas and coffees.

Gifts

Costs are allowable where gifts incorporate a conspicuous advertisement, do not exceed £50 in value (for all gifts made to the same recipient in a year) and are not food, drink, tobacco or tokens or vouchers exchangeable for goods. This could be merchandise branded with the business logo.

Staff Entertainment

Entertaining staff is allowable provided that it is not merely incidental to customer entertaining. Regardless of any deduction allowed against the profits of the business, a tax charge may arise on the employee personally. Employers may need to report the event costs to HM Revenue & Customs (HMRC) on each employee’s form P11D and pay class 1A National Insurance. Generous employers can though opt to pay the Income Tax and National Insurance Contributions on behalf of employees by entering into a PAYE Settlement Agreement (PSA).

To avoid this complicated scenario and to ensure that staff entertainment is allowable, an event would need to meet the following conditions:

- Opening the party to all staff (not only to directors/management)

- Limiting the cost per staff member to £150 per head (inclusive of VAT) per year. In practice, this would mean limiting the cost per general attendee to £150 per head. One would also need to consider any future events in which the limit may be breached, for if the cost per head were to exceed £150, then no tax-deductible expense could be claimed, with a tax charge arising on employees.

To avoid a tax charge, the event would need to meet the additional condition of taking place annually! If an event were to include entertainment for staff as well as customers, the apportionment of expenditure on staff would be fully allowable, whilst the apportionment of expenditure on clients would generally be disallowable (with the exception of any gifts).

Recovering VAT on Entertainment

As a general rule, a business cannot recover input VAT related to client entertainment. VAT incurred on staff entertainment is however recoverable provided the following conditions are met:

1. Entertainment is not only provided for directors/partners

2. Costs incurred are not related to entertaining non-employees. For events which entertain both employees and non-employees, an apportionment of employee-related expenses and VAT would again be made.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Spring Budget 2022

A Targeted Budget

Amid soaring inflation of 6.2% and forecasts of the sharpest fall in living standards since records began (according to the UK’s fiscal watchdog), Rishi Sunak presented a Budget which he argued would support the UK economy, businesses and families in both the short and the medium term. In contrast to the profligate Budgets of very recent times, which were arguably necessary to address a pandemic that affected all areas of the economy from all angles, this was a targeted Budget with a laser beam pointed at the erosion of disposable incomes that is likely to pursue at least in the short term.

The key measures were as follows:

- regarding personal taxes, an increase to the threshold at which an individual will begin to pay NI from 6 July 2022, aligning it with the personal allowance which is set at £12,570 per annum

- regarding employment taxes, the Employment Allowance will be increased by £1,000 from 6 April 2022 to £5,000

- regarding duties, an immediate reduction in duty on diesel and petrol, by 5 pence per litre, for 12 months

- regarding VAT, a cut in the VAT levied on energy efficient upgrades, such as solar panels and energy efficient heating

Rishi Sunak saved the “crowd pleaser”, or “low-tax-Conservative-MPs-and-commentators pleaser” until the end – his virtual rabbit out of the hat, by promising to cut the basic rate of income tax to 19p in the pound in April 2024, conveniently a few weeks before many Tory MPs expect to face a general election. Rishi has kept what looks to be substantial powder for more election-fighting fireworks. Has he done enough for the poorest people in society? Having banked most of the fiscal good news he received – higher than expected growth and tax revenues this year – he could have gone further. He is building up a war chest for the autumn. Momentum politics.

Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

The Taxation of Inter-company Loans

Under the right circumstances, which can of course be shaped, intercompany loans are an effective means of funding further profit or not-for-profit motives. Consider Mr Trader, who is director and sole shareholder of Company T, a trading company. Company T has grown with accumulated profits in excess of £2m, matched by substantial cash balances. Mr Trader has decided to set up a not-for-profit organisation, ReMobly Ltd, aimed at rehabilitating injured athletes back into competitive sport. In addition to Mr Trader, two other directors will be appointed to the board of ReMobly Ltd and each of the three persons will own 33% of the ReMobly Ltd share capital.

ReMobly Ltd is seeking to raise capital to begin its operations and Mr Trader is considering the most apt means of lending money to the not-for-profit organisation. There are three issues which spring to mind…

Loans to participators

In view of the large cash balances that have accumulated in the company, Mr Trader considers lending money from Company T to ReMobly Ltd. CTA10/S455 applies to loans/advances made by a close company to its participator, or an associate of its participator. Broadly, where a close company makes any loan to an individual who is a participator (or an associate of a participator) in the close company, then the close company is due to pay tax under CTA10/S455. The not-for-profit is not classed as an associate of Mr Trader (so far as section 448 of Part 10 of the Corporation Tax Act 2010 is concerned), therefore the loan can be made by Company T without corporation tax implications under CTA10/S455.

It is also important to analyse CTA10/S459, which applies if there are arrangements made by a person whereby a close company makes a loan or advance that is not subject to tax under CTA10/S455, and another person makes a payment to a relevant person who is either a participator of the company or an associate of such a participator. In this case there is a proposed “loan or advance” from a close company. However, there is not then a payment by a person other than Company T to a relevant person who is a participator in Company T or is an associate of such a participator. Indeed ReMobly Ltd is not a relevant person who is an associate of Mr Trader, because a relevant person has to be an individual or a company acting in a fiduciary or representative capacity (CTA10/S455(6)). Therefore the loan can be made without corporation tax implications under CTA10/S459.

Loan write off

There is a possibility that the future activities of ReMobly Ltd will be inadequate to allow for the repayment of the loan made by Company T, under the terms of the loan agreement. If both parties are companies and both are found to be under the common control of another person, company or individual, at any time in the accounting period, then no bad debt relief will be available on the release of the loan, and no taxable credit will arise to the company whose indebtedness is forgiven. Company T and ReMobly Ltd are not under the common control of another person and are therefore not considered to be connected. The debit for the loan write off will be allowable for Company T (most likely as a non-trade loan relationship deficit). The corollary is that a taxable credit will arise to the not-for-profit.

Anti-avoidance

The main anti-avoidance rule will also need to be considered in FA 1996, Sch 9 para 13, the ‘unallowable purposes’ rule. This will deny relief for so much of a debit where the loan or part of the loan is attributable to an unallowable purpose. An unallowable purpose is any purpose which is not amongst the business or other commercial purposes of the company, Company T. If taken literally, this would seem to be cast fairly widely. In general however, if the loan relationship rules are seen to be fairly applied to both parties, HMRC seem content in leaving matters undisturbed.

Whether you’re an existing client or don’t yet use our services, we would be pleased to help you. Contact Mouktaris & Co Chartered Accountants for expert advice or click here to subscribe to our Newsletter.

Negotiating time to pay with HMRC

HMRC has published details of the specific helpline to contact, but it’s not known whether HMRC will change its usual approach to time to pay, for taxpayers who are having difficulty paying.

The following usually needs to be considered when negotiating time to pay with HMRC.

WHEN TO MAKE CONTACT – In general it is advisable to contact HMRC as soon as difficulty making payment is expected. However, HMRC’s systems do not easily facilitate setting up a payment arrangement too far in advance, so the best time to phone HMRC is usually one to two weeks in advance of the due date for payment.

MAKE SURE RETURNS ARE UP TO DATE – HMRC is more amenable to agreeing time to pay if returns are up to date and the correct liability has been established.

CASH FLOW FORECASTS AND BUDGETS – Before phoning HMRC it is advisable to have financial forecasts and a statement of assets and liabilities available. HMRC will expect the taxpayer to make the best offer they can and will not usually make suggestions about the amount it will accept as a regular payment.

HMRC STAFF AUTHORITY TO AGREE TIME TO PAY – HMRC will usually expect to set up a regular monthly payment plan with collection by direct debit. Most HMRC debt management contact centre staff have authority to agree time to pay over a period of up to 12 months. Longer periods can be arranged but usually need to be escalated to more senior HMRC staff.

EXPECT ROBUST QUESTIONING – We don’t know to what extent HMRC staff will be more sympathetic to requests for time to pay in the current environment but in normal circumstances negotiating time to pay can involve what feels like personal and intrusive questioning. It is important to make HMRC aware of all information which might be relevant to the payment difficulties, as calmly and professionally as is possible in what may well be extremely difficult circumstances.

NO AGREEMENT MAY BE BETTER THAN AN UNAFFORDABLE AGREEMENT – It is often better to conclude a phone call to HMRC having failed to reach an agreement than to agree to an arrangement which the business can’t afford. If a time to pay agreement is not kept to it is difficult to get HMRC to reestablish it and HMRC will be more reluctant to make agreements in the future. If circumstances change it is advisable to contact HMRC, before missing any payments, to renegotiate the arrangement. If a formal time to pay arrangement cannot be reached it is usually advisable for the taxpayer to pay what they can when they can as this shows willingness to pay and may delay further enforcement action by HMRC (this approach may not be appropriate if insolvency is likely and further advice should be sought in this situation).

FUTURE TAX LIABILITIES – A standard term of HMRC time to pay agreements is that future tax liabilities are paid in full as they fall due. Where this is not possible it is necessary to contact HMRC again to renegotiate the arrangement to include the new debt. HMRC is often reluctant to agreed repeated requests for time to pay but may be more amenable in the current situation.

WHICH DEBTS TO PRIORITISE – HMRC is usually more willing to consider agreeing time to pay for profits based taxes such as income tax and corporation tax than for taxes such as VAT and employees’ PAYE and national insurance contributions, which businesses are effectively collecting on behalf of the exchequer. The usual advice is to prioritise paying VAT and employer liabilities as HMRC pursues these more actively. We don’t yet know whether this will change in the current situation; there has been some speculation that the Government may be minded to focus assistance on VAT and employer liabilities but no announcement has been made.

LATE PAYMENT PENALTIES – An advantage of a formal time to pay arrangement is that late payment penalties will not be charged if the arrangement is in place at the trigger date for the penalties. We don’t yet know whether HMRC will be more willing to waive late payment penalties in the current situation but the helpline page suggests that the cancellation of penalties will at least be explored.

INTEREST – In normal circumstances HMRC does not waive interest unless the delay in making payment is somehow directly attributable to HMRC. We don’t yet know whether HMRC will be more willing to waive interest in the current situation but the helpline page suggests that the cancelling of interest will at least be explored.

ALTERNATIVE WAYS TO CONTACT HMRC – As well as the COVID-19 helpline HMRC has regular payment helplines. Large businesses with a customer compliance manager should contact that individual. If the debt is a result of a compliance check any anticipated difficulty with making payment should be discussed with the compliance officer, ideally before reaching final settlement.

We are doing everything we can to help our business community. If you would like to discuss how the changes or the coronavirus pandemic may affect you or your business, please do not hesitate to contact us on 020 8952 7717 or use our online enquiry form.

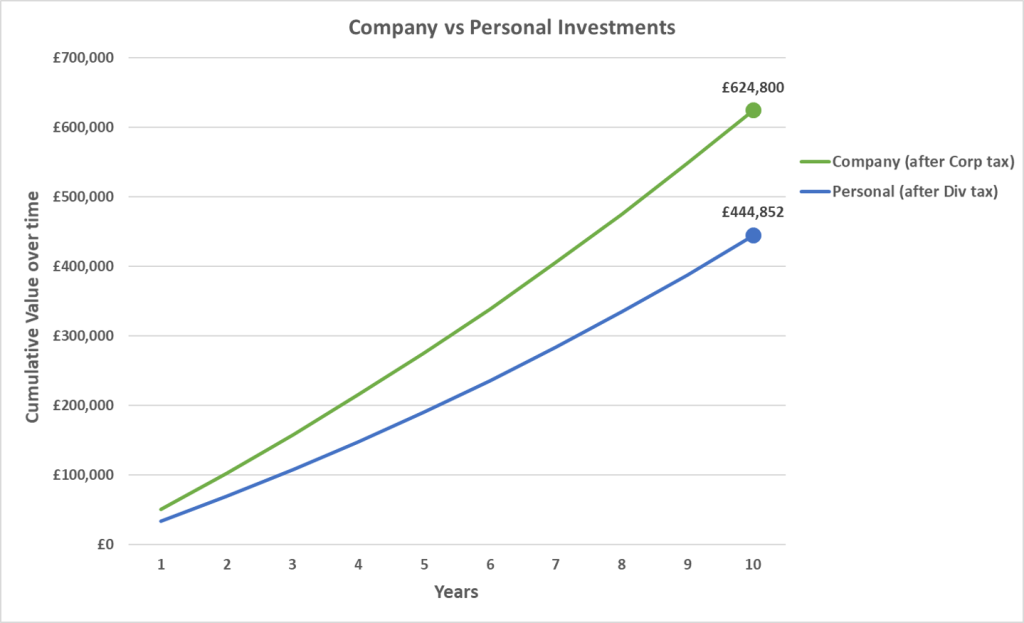

How to Invest Business Profits

With many entrepreneurs accumulating cash in business accounts, the question of “how to invest business profits?” is a favored topic when planning.

Entrepreneurs work hard for their businesses and this short article explores how business funds can work hard- or most effectively, for entrepreneurs.

Let’s take the following scenario: your business is profitable and has accumulated cash. During the years of trading, you have typically drawn an annual salary and dividends of £45,000, a point at which you are paying the basic rates of tax. Now with a stockpile of cash in the business, there are two options through which to invest. Should you personally draw additional funds from the company to invest, or alternatively should you invest from within the corporate structure?

Assume in both cases there is a £50,000 cash surplus in the company. Assume also that this happens every year for the next 10 years.

Personal investment through your ISA

To take the money out of the company, you would pay dividend tax of 32.5% upfront. You (and perhaps your partner) could then invest your money tax-free, say in an ISA wrapper, in which your combined ISA allowances are currently £40,000.

Investment through your Company

Investing the money within the company would mean no upfront dividend tax of 32.5%. You would instead pay corporation tax on the investment income and gains annually, with the caveat that dividends received from stocks and shares are mostly exempt from corporation tax. This is a considerable advantage.

Let’s see how the two strategies fare:

As you can see, investing the money in a limited company yields approximately £180,000 more over a ten-year time horizon. The cost of paying the dividend tax upfront outweighs the benefit of tax-free personal investments. Why should you lose out?

Compounding evidence

You will notice immediately from the graph above that investing your company’s profits in the corporate vehicle, without paying dividend tax, allows the investment to accumulate, or compound, at a faster rate, even after paying corporation tax on investment income and gains.

Sure, if you do not draw the surplus funds from your company you may need to take a 32.5% dividend tax rate hit at a later date, but in the interim you will have generated greater income through compounding.

Caveats

Here we assume constant tax rates at the points of execution, income and realisation. It would be unwise to speculate on domestic policy, but current political trends and economic philosophy may see a conservative government try to enforce its stronghold on previously labour heartlands. Corporation and dividend tax rates could well rise before they fall.

You may find that transaction costs are slightly higher for corporate accounts, chipping away at annual returns. You will need to shop around harder for a broker. Equally personal brokerage accounts tend to be more insurable than corporate accounts.

Investing through a Limited Company

If the preference for investing through a Limited Company has been established, so should the mechanism through which to do so. Yes, you could simply open an investment account for the existing trading company, however there are several reasons why a designated investment company is superior:

- If the trading company runs into legal issues, the investment company will be protected.

- The trading company can be sold off as a standalone vehicle without the need for complex restructuring.

- An investment company will have minimal expenses and overheads, meaning it will be easier to administer for tax purposes (no VAT or payroll requirements).

- A trading company shouldn’t start investing in activities outside its core functions as it could end up becoming reclassified. This may carry tax implications, especially if Entrepreneurs’ Relief is sought.

Whilst the trading company is often the vehicle in which profits have been generated and accumulated, there are tax neutral ways of shifting funds to an investment company, such as lending the cash surplus. There is no obligation to pay back the loan and one can be the sole director of both companies.

A Holding Company

A holding company structure that owns operating companies and receives dividends is favourable. The holding company can own shares in the subsidiary trading companies and can provide centralised corporate control. Additionally, no taxes would be incurred when the trading company is sold.

Special Purpose Vehicle (SPV) for Property

If you want to invest in property it may be a better idea to set up an SPV. This is often a requirement from buy-to-let lenders. If you are looking to acquire a primary residential residence however, personal ownership is often the best way to go.

Don’t let the tax tail wag the investment dog

Your investment goals will seek a level of risk and return that you are comfortable with, regardless of the structure through which you pursue them. The tax wrapper is the “cherry on the top”, though worth a certain percentage of your annual returns. Contact Mouktaris & Co Chartered Accountants for an accountant who understands your investment strategy and can help you plan accordingly.