Category: Advisory

Coronavirus: Help for the Self-employed

Expanding the UK Government’s measures to protect people and businesses from the economic impact of coronavirus, the Chancellor now focused on self-employed individuals (including members of partnerships) whose incomes have suffered.

The Self-employment Income Support Scheme, announced on 26 March 2020, will come as a welcome relief to those in self-employment, who comprise 15.3% of the UK’s workforce. The new scheme will cover 95% of those who are self-employed.

Under the scheme, a grant will be provided to self-employed individuals or partnerships, worth 80% of their profits up to a cap of £2,500 per month. This brings parity with the Coronavirus Job Retention Scheme, announced by the Chancellor last week, where the Government committed to pay up to £2,500 each month in wages of employed workers who are furloughed during the outbreak.

Second lump sum for self-employed [29/05/2020 UPDATE]

The Chancellor has announced a second and final grant to the self-employed who are eligible for the Self-employment Income Support Scheme (SEISS), based on 70% of earnings and capped at £6,570.

HMRC has confirmed the same eligibility criteria will be used to establish self-employed individuals’ entitlement to a further SEISS grant; the grant will be 70% rather than 80% of average earnings for three months and the maximum amount will be capped at £6,570, down from the £7,500 for the first grant. Applications will open in August and HMRC expects to publish further guidance on 12 June. As with the first claim, the second claim has to made by the taxpayer and cannot be made by agents.

QUALIFYING FOR THE SCHEME

- Self-employed or a member of a partnership

- Lost trading or partnership trading profits due to coronavirus (Covid-19)

- Filed a Tax Return for 2018-2019 as self-employed or a member of a trading partnership

- Eligible individuals who have not yet submitted 2018-2019 Tax Returns will have another four weeks to file in order to become eligible for this scheme (at time of writing a deadline of 23 April 2020).

- Not applicable to anyone who started trading in 2019-2020.

- Traded in 2019-2020 and were trading up until the point of application (or would be except for coronavirus)

- Intend to continue to trade in the tax year 2020-2021

- Trading profits of £50,000 or less and more than half of your total income come from self-employment. This can be with reference to at least one of the following conditions:

- Trading profits and total income in 2018-2019

- Average trading profits and total income across up to the three years between 2016-2017, 2017-2018 and 2018-2019.

We are doing everything we can to help our business community. If you would like to discuss how the changes or the coronavirus pandemic may affect you or your business, please do not hesitate to contact us on 020 8952 7717 or use our online enquiry form.

Negotiating time to pay with HMRC

HMRC has published details of the specific helpline to contact, but it’s not known whether HMRC will change its usual approach to time to pay, for taxpayers who are having difficulty paying.

The following usually needs to be considered when negotiating time to pay with HMRC.

WHEN TO MAKE CONTACT – In general it is advisable to contact HMRC as soon as difficulty making payment is expected. However, HMRC’s systems do not easily facilitate setting up a payment arrangement too far in advance, so the best time to phone HMRC is usually one to two weeks in advance of the due date for payment.

MAKE SURE RETURNS ARE UP TO DATE – HMRC is more amenable to agreeing time to pay if returns are up to date and the correct liability has been established.

CASH FLOW FORECASTS AND BUDGETS – Before phoning HMRC it is advisable to have financial forecasts and a statement of assets and liabilities available. HMRC will expect the taxpayer to make the best offer they can and will not usually make suggestions about the amount it will accept as a regular payment.

HMRC STAFF AUTHORITY TO AGREE TIME TO PAY – HMRC will usually expect to set up a regular monthly payment plan with collection by direct debit. Most HMRC debt management contact centre staff have authority to agree time to pay over a period of up to 12 months. Longer periods can be arranged but usually need to be escalated to more senior HMRC staff.

EXPECT ROBUST QUESTIONING – We don’t know to what extent HMRC staff will be more sympathetic to requests for time to pay in the current environment but in normal circumstances negotiating time to pay can involve what feels like personal and intrusive questioning. It is important to make HMRC aware of all information which might be relevant to the payment difficulties, as calmly and professionally as is possible in what may well be extremely difficult circumstances.

NO AGREEMENT MAY BE BETTER THAN AN UNAFFORDABLE AGREEMENT – It is often better to conclude a phone call to HMRC having failed to reach an agreement than to agree to an arrangement which the business can’t afford. If a time to pay agreement is not kept to it is difficult to get HMRC to reestablish it and HMRC will be more reluctant to make agreements in the future. If circumstances change it is advisable to contact HMRC, before missing any payments, to renegotiate the arrangement. If a formal time to pay arrangement cannot be reached it is usually advisable for the taxpayer to pay what they can when they can as this shows willingness to pay and may delay further enforcement action by HMRC (this approach may not be appropriate if insolvency is likely and further advice should be sought in this situation).

FUTURE TAX LIABILITIES – A standard term of HMRC time to pay agreements is that future tax liabilities are paid in full as they fall due. Where this is not possible it is necessary to contact HMRC again to renegotiate the arrangement to include the new debt. HMRC is often reluctant to agreed repeated requests for time to pay but may be more amenable in the current situation.

WHICH DEBTS TO PRIORITISE – HMRC is usually more willing to consider agreeing time to pay for profits based taxes such as income tax and corporation tax than for taxes such as VAT and employees’ PAYE and national insurance contributions, which businesses are effectively collecting on behalf of the exchequer. The usual advice is to prioritise paying VAT and employer liabilities as HMRC pursues these more actively. We don’t yet know whether this will change in the current situation; there has been some speculation that the Government may be minded to focus assistance on VAT and employer liabilities but no announcement has been made.

LATE PAYMENT PENALTIES – An advantage of a formal time to pay arrangement is that late payment penalties will not be charged if the arrangement is in place at the trigger date for the penalties. We don’t yet know whether HMRC will be more willing to waive late payment penalties in the current situation but the helpline page suggests that the cancellation of penalties will at least be explored.

INTEREST – In normal circumstances HMRC does not waive interest unless the delay in making payment is somehow directly attributable to HMRC. We don’t yet know whether HMRC will be more willing to waive interest in the current situation but the helpline page suggests that the cancelling of interest will at least be explored.

ALTERNATIVE WAYS TO CONTACT HMRC – As well as the COVID-19 helpline HMRC has regular payment helplines. Large businesses with a customer compliance manager should contact that individual. If the debt is a result of a compliance check any anticipated difficulty with making payment should be discussed with the compliance officer, ideally before reaching final settlement.

We are doing everything we can to help our business community. If you would like to discuss how the changes or the coronavirus pandemic may affect you or your business, please do not hesitate to contact us on 020 8952 7717 or use our online enquiry form.

Coronavirus: An Unprecedented Economic Intervention: Coronavirus Job Retention Scheme, VAT Deferral, Income Tax Deferral and Universal Credit

AN UNPRECEDENTED ECONOMIC INTERVENTION

In addition to measures announced in the Budget on 11 March 2020 and subsequently on 17 and 18 March 2020 (see our news releases here and here respectively), the Chancellor’s announcement on 20 March 2020 of a far-reaching package of measures allows businesses in this country to stand by their employees at a time of national emergency. Though this is not a helicopter money policy which would indiscriminately and radically boost the back pocket of workers and employers alike, such direct action by Government to encourage continued employment of people is a really good start. It is though to be read against the sombering order for all cafés, pubs and restaurants (dine-in, not takeaway), cinemas, gyms, nightclubs and leisure centres across the UK, to temporarily close.

Much of the detail is still being worked out and we expect more information to follow, including potentially wider measures to support the self-employed and the freelance economy.

You can continue to follow the latest advice and guidance from government for businesses on its coronavirus pages.

A summary of the practical measures announced by the Chancellor on 20 March 2020:

CORONAVIRUS JOB RETENTION SCHEME (CJRS)

If an employer cannot maintain its current workforce because its operations have been severely affected by coronavirus (Covid-19), the employer can furlough employees and apply for a grant that covers 80% of the usual monthly wage costs, up to £2,500 a month, plus the associated Employer National Insurance contributions and minimum automatic enrolment employer pension contributions on that wage. The scheme is designed to protect the UK economy by encouraging continued employment.

Timing

This is a temporary scheme in place for 3 months starting from 1 March 2020, but it may be extended if necessary and employers can use this scheme anytime during this period. The scheme, open to any employer in the United Kingdom, will cover the cost of wages backdated to 1 March 2020 and will be open on 20 April 2020 [UPDATE]. It can include workers who were in employment on 28 February.

Claiming

To claim under the scheme employers will need to:

- designate affected employees as ‘furloughed workers’, and notify employees of this change. Changing the status of employees remains subject to existing employment law and, depending on the employment contract, may be subject to negotiation.

- submit information to HMRC about the employees that have been furloughed and their earnings through a new online portal. HMRC will set out further details on the information required.

- HMRC will reimburse 80% of furloughed workers wage costs, up to a cap of £2,500 per month. This is in addition to the £4,000 employer’s national insurance allowance.

While HMRC is working urgently to set up a system for reimbursement, we understand existing systems are not set up to facilitate payments to employers. Business that need short-term cash flow support, may benefit from the VAT deferral announced below and may also be eligible to apply for a Coronavirus Business Interruption Loan.

Directors [06/04/2020 UPDATE]

As office holders, salaried company directors are eligible to be furloughed and receive support through this scheme. Company directors owe duties to their company which are set out in the Companies Act 2006. Where furloughed directors need to carry out particular duties to fulfil the statutory obligations they owe to their company, they may do so provided they do no more than would reasonably be judged necessary for that purpose, for instance, they should not do work of a kind they would carry out in normal circumstances to generate commercial revenue or provides services to or on behalf of their company.

New cut-off date [15/04/2020 UPDATE]

The government has announced a major change to the CJRS, moving the cut-off date from 28 February to 19 March. To qualify for the grant, the employer must now have created and started a PAYE payroll scheme on or before 19 March 2020.

Employees who were employed on 28 February 2020 and on payroll (ie notified to HMRC on an RTI submission on or before 28 February) and who were made redundant or stopped working for the employer after that and prior to 19 March 2020, can also qualify for the scheme if the employer re-employs them and puts them on furlough.

The government published further details on the intended mechanics of the scheme on 26 March 2020 [06/04/2020 and 15/04/2020 UPDATES].

Chancellor extends furlough scheme until October [12/05/2020 UPDATE]

In a boost to millions of jobs and businesses, Rishi Sunak said the furlough scheme would be extended by a further four months to October 2020, with workers continuing to receive 80% of their current salary. The proposal is for employer payments to substitute the contribution the government is currently making, ensuring that staff continue to receive 80% of their salary, up to £2,500 a month.

VAT PAYMENTS

The next quarter of VAT payments will be deferred, meaning businesses will not need to make VAT payments until the end of June 2020. Businesses will then have until the end of the 2020-21 tax year (31 March 2021) to settle any liabilities that have accumulated during the deferral period.

The deferral applies automatically and businesses do not need to apply for it. VAT refunds and reclaims will be paid by the government as normal.

Taxpayers will need to cancel their Direct Debit for VAT in order to avoid automatic payments from being made. This will of course need to be re-instigated following the deferral period.

VAT Returns must still be filed on time.

INCOME TAX PAYMENTS ON ACCOUNT

Income Tax payments due on 31 July 2020 under the Self-Assessment system will be deferred to 31 January 2021. This is an automatic offer with no applications required. No penalties or interest for late payment will be charged in the deferral period.

This measure will benefit self-employed persons who have historically filed Tax Returns, but self-employed individuals who began trading after 5 April 2019 will not see an immediate benefit.

UNIVERSAL CREDIT

The measures announced by the government thus far fall short of shoring up the previously thriving self-employed- or freelance, economy. The policies seem to be resigned to the fact that some job losses are inevitable, but those affected will be helped to an extent by a marginally more generous welfare system- equivalent to an annual increase of £1,000.

One group of economic agents that will not gain any protection from the new measures is freelancers on relatively high incomes, if they have savings or other household income that would make them ineligible for Universal Credit.

We are doing everything we can to help our business community. If you would like to discuss how the changes or the coronavirus pandemic may affect you or your business, please do not hesitate to contact us on 020 8952 7717 or use our online enquiry form.

Coronavirus: Residential Property, Commercial Property and IR35

MORTGAGE AND RENT HOLIDAY – RESIDENTIAL PROPERTY

Residential tenants can apply for a three-month payment holiday from their landlord. As per the government’s announcement on 18 March 2020, no one can be evicted from their home or have their home repossessed over the next three months. The Residential Landlords Association and the National Landlords Association both reassuringly welcomed the news.

In turn mortgage borrowers (who are individuals) can apply for a three-month payment holiday from their lender. Both residential and buy-to-let mortgages are eligible for the holiday. It is important to remember that borrowers still owe the amounts that they don’t pay as a result of the payment holiday and that interest will continue to be charged on the amount they owe.

In practice:

- Tenants should continue to pay rent where possible.

- Should a tenant fall in arrears, it is up to the landlord and tenant to come to a sensible agreement. The Tenancy Agreement and evidence of hardship can be used as a basis for agreement.

- Where the three-month month payment holiday doesn’t apply, lenders may not be sympathetic and so if tenants withhold payments of rent, landlords will have to take action to recover it.

- Landlords would face practical hurdles in finding a new tenant in this current climate, not least because the government is advising the public to, where possible, “delay moving to a new house while measures are in place to fight coronavirus”.

EVICTION PROTECTION – COMMERCIAL PROPERTY

Commercial tenants who cannot pay their rent because of coronavirus will be protected from eviction, the government announced on 23 March 2020. This protection may however encourage tenants not to pay rents for the coming quarter or to seek reductions. A corresponding relief may be needed to protect landlords from their lenders.

In practice:

- Rent is due and remains governed by the lease agreement.

- Landlords and tenants are already having conversations and reaching voluntary arrangements about rental payments.

- An issue for property businesses is likely to be cashflow. Tenants may not be paying in full, while lenders are still requiring interest payments to be made. Property developers will likely be unable to sell property in the current climate.

- Businesses can access funding through, for example, the “Coronavirus Business Interruption Loan Scheme”. The scheme has been designed precisely for the purpose of enabling businesses to continue meeting overheads such as rent.

- Landlords would more-likely-than-not face even higher hurdles in finding a new, good-quality tenant in this current climate.

IR35 CHANGES HAVE BEEN POSTPONED TO APRIL 2021 DUE TO CORONAVIRUS

The Government has announced that it will be deferring new rules affecting contractors working for the private sector, directly or through an agency, that were due to come into force from 6th April 2020 until 6th April 2021.

The changes which would have affected all contractors working for medium or larger organisations, had initially been confirmed in The Budget.

The chief secretary said: ‘I can also announce that the government are postponing the reforms to the off-payroll working rules IR35 from April 2020 to 6 April 2021. The government will therefore not move the original resolution tonight, but it will shortly table an additional resolution confirming that we will reintroduce the off-payroll working rules provisions by amending the Bill, with a commencement date of the 6 April 2021. This is a deferral in response to the ongoing spread of covid-19 to help businesses and individuals. This is a deferral, not a cancellation, and the government remain committed to reintroducing this policy to ensure that people who are working like employees, but through their own limited company, pay broadly the same tax as those employed directly.’

What you should do next

The impact of this deferral will depend on your circumstances and actions taken to date by the company or agency you work for, but generally you should consider:

- Reviewing the actions, you have taken and see if these are impacted by the deferral. For example, if you have started an insolvency process on the basis that you no longer need your company you may need to defer this.

- Talking to the organisation you work for to see if the deferral has/will change their approach.

- Reviewing any determinations sent out by your agency or firm in anticipation of the change. The deferral will mean that you will be responsible for determining whether your contract is inside or outside IR35 for a further 12 months.

- Most importantly, talking to your accountant. The Government is issuing guidance regularly as it tries to keep pace with the current situation, meaning a review of your own circumstances is more important than ever.

If you would like to discuss how the IR35 changes or the coronavirus pandemic may affect you or your business, please do not hesitate to contact us on 020 8952 7717 or use our online enquiry form.

Coronavirus: SSP, Business Rates and the Coronavirus Interruption Loan Scheme

SUPPORT FOR BUSINESSES THROUGH THE CORONAVIRUS BUSINESS INTERRUPTION LOAN SCHEME (CBILS)

A new temporary Coronavirus Business Interruption Loan Scheme, delivered by the British Business Bank, will launch next week to support businesses to access bank lending and overdrafts. The government will provide lenders with a guarantee of 80% on each loan to give lenders further confidence in continuing to provide finance to SMEs. The government will not charge businesses or banks for this guarantee, and the Scheme will support loans of up to £5 million in value. Businesses can access the first 6 months of that finance interest free, as government will cover the first 6 months of interest payments.

Further details on the scheme can be found on the government webpage which, as you can see, is in the process of being updated. Accredited lenders are set out here.

This type of loan may be helpful for businesses that continue to pay overheads against little or no income stream, where income streams are expected to resume following a period of interruption (e.g. Covid-19). Please reach out if you are unsure of how your business may benefit. If you believe that this scheme could benefit your business, we urge you to contact your banking or finance relationship manager to flag your interest at this relatively early stage.

Personal Guarantees

Insufficient security is no longer a condition to access the scheme. Lenders will not take personal guarantees for facilities below £250,000. For facilities above £250,000 personal guarantees may still be required, at a lender’s discretion, though will excllude the Principal Private Residence (PPR).

Companies claiming R&D Tax Credits

The CBILS is deemed to be a Notified State Aid (an EU-approved government subsidy), as are Research & Development (R&D) tax credits. A company cannot have two Notified State Aids for the same project and therefore companies already in receipt of R&D tax credits may be restricted from claiming loan scheme support as well (and vice versa).

Viability [21/04/2020 UPDATE]

Borrowing proposals must be viable were it not for Covid-19. Viability is tested for loans above £30,000. For small and medium-sized businesses, accumulated losses at 31 December 2019 cannot exceed 50% of subscribed share capital, though these rules do not apply to businesses less than three years old. For larger businesses the EBITDA/interest ratio must be more than 1.0 and the debt/equity ratio less than 7.5.

Evidence Requirements Relaxed [29/04/2020 UPDATE]

To speed up the provision of finance to small and medium-sized businesses under CBILS, the largest seven SME lenders (Barclays Bank UK, Danske Bank, HSBC, Lloyds Bank, NatWest, Santander and Virgin Money) have stated that rather than relying on businesses providing forecasts and business plans in applications, lenders will use their own information. While the exact details of the changes are still to be released, the moves should make the scheme easier to access and make the application process quicker. However, businesses should still assess carefully the implications of taking on debt finance and be comfortable that this is the right solution for them at this time.

SUPPORT FOR BUSINESSES THAT PAY BUSINESS RATES

- The retail discount is 100% for 2020-21 for properties with a rateable value below £51,000. Businesses in this category should pay no rates for the year beginning April 2020. Please review your direct debit arrangements if necessary.

- No measures have yet been announced for businesses with a rateable value above £51,000 though these could soon follow.

- Businesses that received the retrospective retail discount in the 2019 to 2020 tax year will be rebilled by their local authority as soon as possible. This has already taken effect for some local authorities. We advise our clients to request, in writing, that any credit in your business rates account is paid back to the business by BACS, rather than offset against future liabilities. You should contact your local authority for advice on executing this.

- A £25,000 grant will be provided to retail, hospitality and leisure businesses operating from smaller premises, with a rateable value between £15,000 and £51,000. Details on the mechanism of this measure are yet to be released by the government.

- A £10,000 grant (previously £3,000) is available for businesses that do not pay rates. Details on the mechanism of this measure are yet to be released by the government.

Any enquiries on eligibility for, or provision of, the reliefs should be directed to the relevant local authority. Guidance for local authorities on the business rates holiday will be published by 20 March.

SUPPORT FOR BUSINESSES WHO ARE PAYING SICK PAY (SSP) TO EMPLOYEES

- The cost of providing 14 days of SSP per employee will be refunded by the government in full. The government will work with employers over the coming months to set up the repayment mechanism for employers as soon as possible.

- SSP will be payable from day 1 instead of day 4.

- Employers should maintain records of staff absences and payments of SSP, but employees will not need to provide a GP fit note.

Remember that by law, employers must pay Statutory Sick Pay (SSP) to employees and workers when they meet the following eligibility conditions (agency, casual and zero-hours workers can also get SSP):

- they’ve been off sick for at least 4 days in a row, including non-working days (reduced to 1 day for Covid-19)

- they earn on average at least £118 per week, before tax

- they’ve told their employer within any deadline the employer has set or within 7 days

Another option is to tell employees to take their holiday entitlement now whilst your business closes temporarily. Please refer to this guidance from ACAS. We are also available to answer employment-related queries. For our clients who subscribe to our HMRC investigation service, we offer access to legal employment advice.

If you are considering temporarily closing the workplace and reducing staff hours or laying off staff, it’s important to talk with staff as early as possible and throughout the closure. Unless it says in the contract or is agreed otherwise, you will still need to pay employees for this time.

SUPPORT FOR BUSINESSES PAYING TAX

All businesses and self-employed people in financial distress, and with outstanding tax liabilities, may be eligible to receive support with their tax affairs through HMRC’s Time To Pay service. These arrangements are agreed on a case-by-case basis and are tailored to individual circumstances and liabilities. If you are concerned about being able to pay your tax due to Covid-19, call HMRC’s helpline on 0800 0159 559.

Our page on Negotiating time to pay with HMRC is a useful first port of call.

INSURANCE

Businesses that have cover for both pandemics and government-ordered closure should be covered, as the government and insurance industry confirmed on 17 March 2020 that advice to avoid pubs, theatres etc is sufficient to make a claim. Insurance policies differ significantly, so businesses are encouraged to check the terms and conditions of their specific policy and contact their providers. Most businesses are unlikely to be covered, as standard business interruption insurance policies are dependent on damage to property and will exclude pandemics.

We are here to support you, and we will do all that we can to ensure you receive the guidance you need.

We wish our entire community the very best for your health and wellbeing during this challenging period.

How to Invest Business Profits

With many entrepreneurs accumulating cash in business accounts, the question of “how to invest business profits?” is a favored topic when planning.

Entrepreneurs work hard for their businesses and this short article explores how business funds can work hard- or most effectively, for entrepreneurs.

Let’s take the following scenario: your business is profitable and has accumulated cash. During the years of trading, you have typically drawn an annual salary and dividends of £45,000, a point at which you are paying the basic rates of tax. Now with a stockpile of cash in the business, there are two options through which to invest. Should you personally draw additional funds from the company to invest, or alternatively should you invest from within the corporate structure?

Assume in both cases there is a £50,000 cash surplus in the company. Assume also that this happens every year for the next 10 years.

Personal investment through your ISA

To take the money out of the company, you would pay dividend tax of 32.5% upfront. You (and perhaps your partner) could then invest your money tax-free, say in an ISA wrapper, in which your combined ISA allowances are currently £40,000.

Investment through your Company

Investing the money within the company would mean no upfront dividend tax of 32.5%. You would instead pay corporation tax on the investment income and gains annually, with the caveat that dividends received from stocks and shares are mostly exempt from corporation tax. This is a considerable advantage.

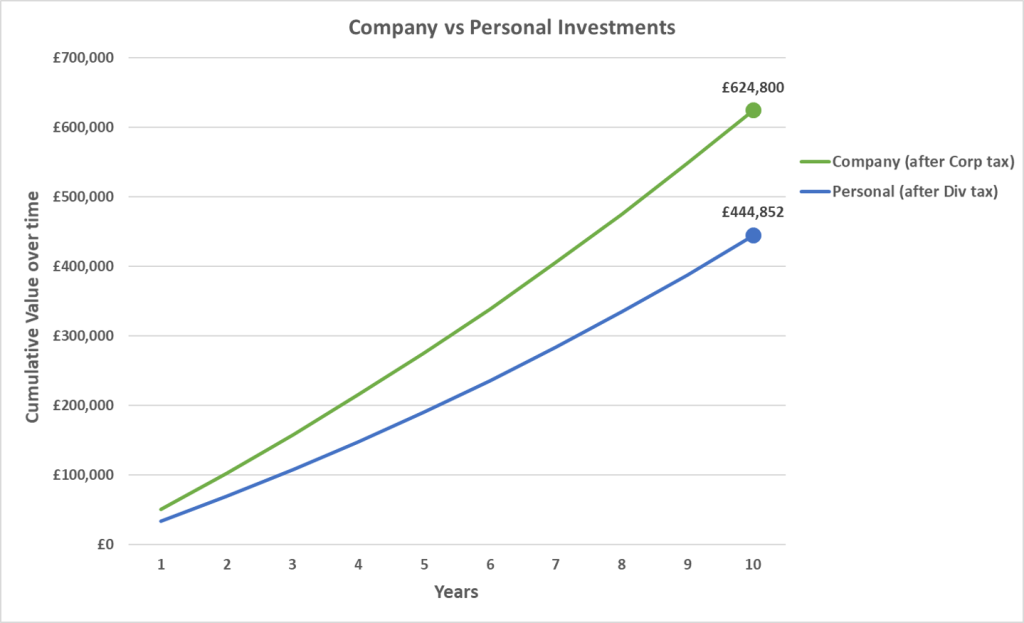

Let’s see how the two strategies fare:

As you can see, investing the money in a limited company yields approximately £180,000 more over a ten-year time horizon. The cost of paying the dividend tax upfront outweighs the benefit of tax-free personal investments. Why should you lose out?

Compounding evidence

You will notice immediately from the graph above that investing your company’s profits in the corporate vehicle, without paying dividend tax, allows the investment to accumulate, or compound, at a faster rate, even after paying corporation tax on investment income and gains.

Sure, if you do not draw the surplus funds from your company you may need to take a 32.5% dividend tax rate hit at a later date, but in the interim you will have generated greater income through compounding.

Caveats

Here we assume constant tax rates at the points of execution, income and realisation. It would be unwise to speculate on domestic policy, but current political trends and economic philosophy may see a conservative government try to enforce its stronghold on previously labour heartlands. Corporation and dividend tax rates could well rise before they fall.

You may find that transaction costs are slightly higher for corporate accounts, chipping away at annual returns. You will need to shop around harder for a broker. Equally personal brokerage accounts tend to be more insurable than corporate accounts.

Investing through a Limited Company

If the preference for investing through a Limited Company has been established, so should the mechanism through which to do so. Yes, you could simply open an investment account for the existing trading company, however there are several reasons why a designated investment company is superior:

- If the trading company runs into legal issues, the investment company will be protected.

- The trading company can be sold off as a standalone vehicle without the need for complex restructuring.

- An investment company will have minimal expenses and overheads, meaning it will be easier to administer for tax purposes (no VAT or payroll requirements).

- A trading company shouldn’t start investing in activities outside its core functions as it could end up becoming reclassified. This may carry tax implications, especially if Entrepreneurs’ Relief is sought.

Whilst the trading company is often the vehicle in which profits have been generated and accumulated, there are tax neutral ways of shifting funds to an investment company, such as lending the cash surplus. There is no obligation to pay back the loan and one can be the sole director of both companies.

A Holding Company

A holding company structure that owns operating companies and receives dividends is favourable. The holding company can own shares in the subsidiary trading companies and can provide centralised corporate control. Additionally, no taxes would be incurred when the trading company is sold.

Special Purpose Vehicle (SPV) for Property

If you want to invest in property it may be a better idea to set up an SPV. This is often a requirement from buy-to-let lenders. If you are looking to acquire a primary residential residence however, personal ownership is often the best way to go.

Don’t let the tax tail wag the investment dog

Your investment goals will seek a level of risk and return that you are comfortable with, regardless of the structure through which you pursue them. The tax wrapper is the “cherry on the top”, though worth a certain percentage of your annual returns. Contact Mouktaris & Co Chartered Accountants for an accountant who understands your investment strategy and can help you plan accordingly.

Non-resident Taxation of Income from UK Property

Finance Act 2019 has introduced two changes to the taxation of non-resident income from UK property:

- From 6 April 2019, disposals of direct or indirect interests in UK land are brought into the Territorial scope of charge; and

- From 6 April 2020, income from a UK property business is moved out of the charge to income tax and brought into the charge to corporation tax.

Background: the position until 5 April 2020

Non-UK resident companies have been subject to income tax in respect of property income arising in the UK. Tax has been chargeable at the basic rate of 20%. These companies are required to complete a Non-resident Company Income Tax Return (SA700).

Finance Act 2019

Coming into effect from 6 April 2020, income from a non-resident UK property business will now be subject to corporation tax rather than income tax. The corporation tax rate is currently charged at 19%: 1% point lower than the equivalent income tax rate. The details of profits to be charged with corporation tax will be included on a company tax return form CT600, as opposed to the SA700.

From an administrative point of view, the annual company tax return will include details of both UK property business income and any property disposals for the accounting period as a whole, on which corporation tax will be due. The filing deadline is 12 months after the end of the accounting period, though in practice, this will be filed 9 months after the end of the accounting period: the point at which any corporation tax is due.

Property losses and allowable deductions

Profits and losses will accordingly be drawn up under corporation tax principles according to the rules of CTA 2009 Part 4.

Loan relationships or derivative contracts that the non-resident company is party to for the purposes of its UK property business are also brought into the charge to corporation tax.

For companies that have net deductible interest and financing costs of over £2 million per annum, there will be a limit to the amount that the company can deduct: the Corporate Interest Restriction.

Transitional rules

UK property business income tax losses carried forward at the point of transition, 6 April 2020, will be grandfathered and therefore deductible under corporation tax rules against future income of the property business.

Capital allowance balances will transfer between the two regimes in such a way as to produce no balancing allowances or charges.

Notably, if a company’s only source of UK income after 6 April 2020 is expected to be income from the UK property business, no Income Tax payments on account for 2020/2021 and future tax years will be required. Similarly, if a credit balance remains in the company’s Income Tax account after all Income Tax liabilities for 2019/2020 and earlier years have been settled, the credit balance will be repaid to the company.

Annual Tax on Enveloped Dwellings (ATED)

ATED on residential properties owned through a corporate structure with a value of more than £500,000 continues to be unchanged following the Finance Act 2019. As ever, ATED can be relieved in full for residential property that is let to a third party on a commercial basis and isn’t, at any time, occupied (or available for occupation) by anyone connected with the owner. Other reliefs can be claimed as per sections 30 to 41 of the ATED technical guidance.

Capital Gains Tax (CGT) on UK property

Non-residents, both individuals and companies, are taxed on almost all gains made on disposals of UK residential properties. Since 6 April 2019, non-UK residents who make an indirect disposal of an interest in UK land will also be brought into the Territorial scope of charge, with the new s1A of TCGA 1992 Part 1. Indirect disposals can for example be disposals of shares in a non-UK entity that derives at least 75% of its value from UK land, provided that the person making the disposal has an investment of at least 25% in that company. The scope of taxation for non-residents has been extended from targeting UK residential property specifically, to now including commercial property and disposals of shares in so-called ‘property rich’ entities. Disposals will be reported in the annual company tax return.

Mouktaris & Co have experience in helping clients navigate the regulatory, accounting and tax matters of property businesses. Our team can review your corporate structure and advise on whether it may be beneficial to de-envelope or restructure in other ways, to take heed of an almost even UK vs non-UK playing field. This will include reviewing potential capital gains tax, stamp duty and inheritance tax liabilities as well as commercial considerations of raising finance and banking relationships in the UK and offshore.

Contact Mouktaris & Co Chartered Accountants to find out how we can help your property rental business.

- ‹ Previous

- 1

- 2